Category: Workplace

-

Why It’s Time to End ‘Retirement’ as We Know It

The traditional concept of retirement and working age is facing a significant shift. As people live longer and pension ages rise, the idea of a fixed working age bracket is becoming increasingly irrelevant. In OECD countries, an average of 23%…

-

The Rise of Shadow AI is a Double-Edged Sword for Corporate Innovation

In the ever-evolving landscape of corporate technology, a new phenomenon is emerging that’s both thrilling and concerning: Shadow AI. This term refers to the growing trend of employees using consumer-grade AI tools without official company approval, a practice that’s rapidly…

-

How AI is Changing the Consulting Game

As artificial intelligence transforms the consulting industry, the traditional pricing model based on billable hours is quickly becoming obsolete. With AI cutting the time needed for many consulting tasks, clients are demanding a shift to value-based pricing. That’s the essential…

-

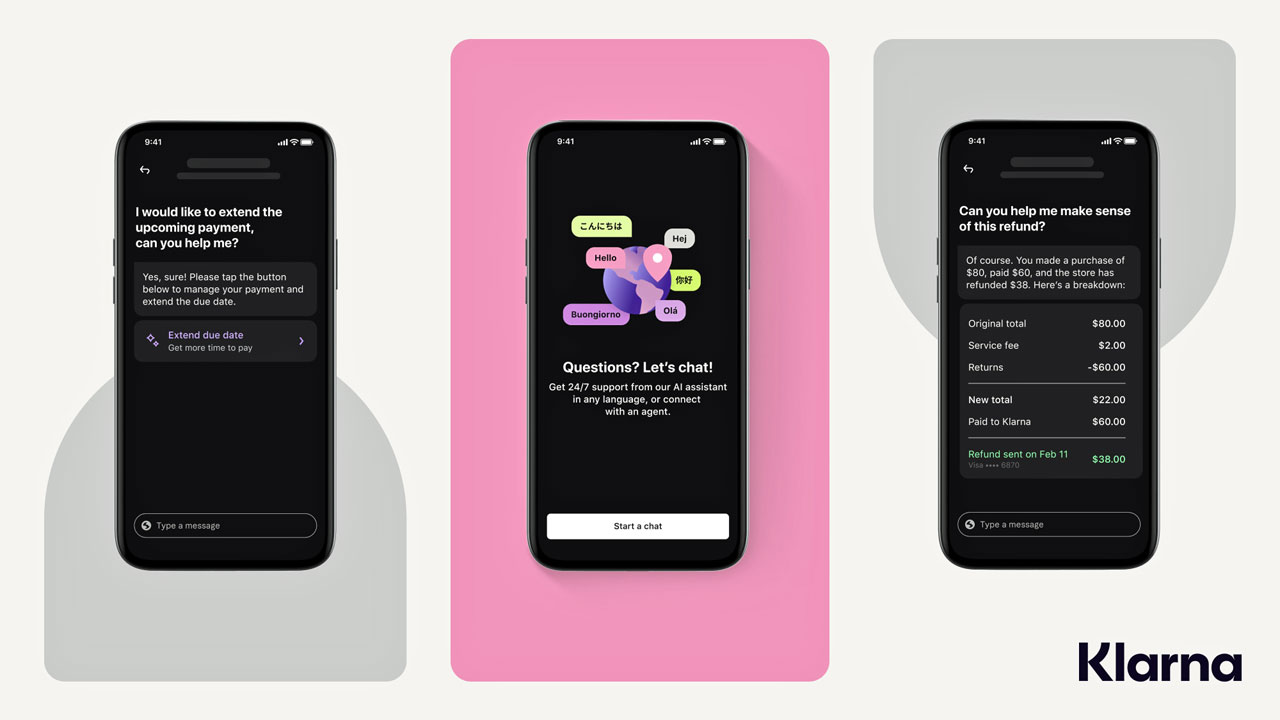

A Balanced Approach to AI Integration: Lessons From Klarna’s Customer Service Success

Klarna, a Swedish international fintech company, has introduced an AI assistant developed in collaboration with OpenAI, the maker of ChatGPT. Klarna says it has significantly transformed its customer service operations. In a press release on 27 February, Klarna itemised an…

-

Digital hoarders: we’ve identified four types – which are you?

How many emails are in your inbox? If the answer is thousands, or if you often struggle to find a file on your computer among its cluttered hard drive, then you might be classed as a digital hoarder. In the…